Rethinking market hours: why Europe should follow behaviour, not headlines

Calls to extend equity trading hours have resurfaced with force as major US venues – including Nasdaq, CBOE and NYSE – push toward near round-the-clock access. The message is gaining traction: more access means more opportunity. But for Europe, already home to the longest primary trading day in global equities, the question isn’t just whether we can follow suit, but whether we should.

Rather than mirroring the US approach outright, now is the time to ask what’s driving these changes and whether similar conditions exist in Europe.

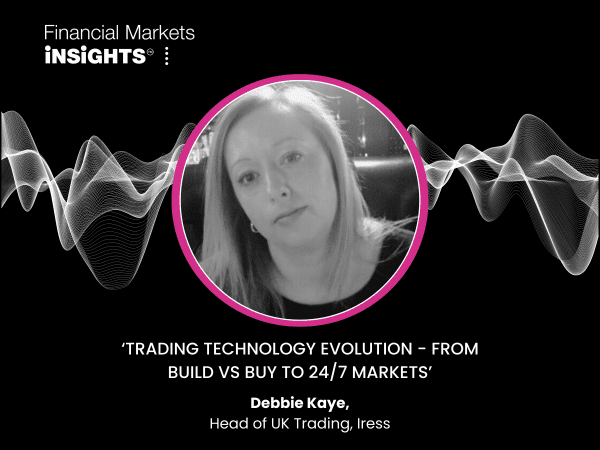

In this Financial Markets Insight article, James Baugh, Head of European Market Structure, TD Securities, and Chris Collins, Senior Trader, Lazard Asset Management, challenge the assumption that more time on the clock automatically leads to better outcomes.

They bring distinct but complementary perspectives: James with a focus on market structure, Chris from the vantage point of institutional execution. James argues that any conversation on trading hours must start with Europe’s liquidity patterns and the diverse participant mix. Building on that, Chris stresses the need to evaluate changes through the lens of client outcomes.

Both agree: Europe must resist the urge to follow US headlines. Reform must be grounded in how this market actually functions and be built to deliver lasting value for investors.

Challenging the headlines, with the facts

The debate around extended hours in Europe has been shaped by headline-grabbing developments in the US. But the headlines rarely tell the full story. While some US venues now offer access across 24/5 windows, only a small percentage of trading takes place outside the core 6.5-hour session. Pre-market volumes typically account for around 4 percent of total activity; post-market volumes around 2 percent.

Chris is quick to challenge the hype. “It’s easy to assume that 24-hour access equals round-the-clock activity,” he says. “But when you drill into the numbers, it’s a rounding error. The real liquidity is still concentrated during the main session. The rest is mostly noise.”

Even crypto, which is often cited as the benchmark for 24/7 retail participation, tends to follow traditional trading rhythms. “There’s a lot of talk about crypto leading the way on 24/7 access,” James notes, “But even there, Bitcoin turnover closely mirrors Nasdaq activity patterns, especially when US futures reopen on Sunday nights.”

Their point is clear: policy should follow real behavioural data, not headlines. “Decisions around market structure should be led by observable behaviour, not perception,” says James. “Headline trends don’t always reflect how participants actually interact with markets.”

Understanding the dynamics: when and where liquidity forms in Europe

Europe’s primary markets operate the longest continuous equity trading day in the world, with most of them running at eight and a half hours. Yet market activity is far from evenly spread.

In many markets, over half of daily turnover occurs after the US opens. For example, FTSE-listed stocks see around 62 percent of trading between 14:30 and 16:30, while nearly 50 percent of Oslo Børs volume takes place in the final 55 minutes of the session – in the short overlap with the US. “That tells you something about where real liquidity comes from,” notes James.

By contrast, the US move towards longer hours has been largely driven by retail demand, particularly from Asian investors trading a narrow set of high-profile stocks. “That demand profile simply doesn’t exist in Europe to the same degree,” he says. “Without that driver, it’s hard to see the case for extending hours in the same way.”

Chris agrees: “We’re open longer and trading a fraction of the volume,” he notes. “You look at the US, they trade ten times the volume in a shorter window. So why are we open for eight and a half hours? It doesn’t translate to better outcomes for clients, it just spreads liquidity thinner.”

International comparisons offer useful reference points. When Norway reduced its trading hours, overall volume remained stable. In contrast, Japan’s recent move to slightly extend its trading day has not meaningfully boosted trading activity. These examples reinforce a central point: effective market structure is not simply a function of hours open, but of aligning those hours with when liquidity naturally forms.

That’s why, rather than extending hours, both suggest there is a stronger case for a later start to the trading day – concentrating liquidity, reducing trading costs and improving execution quality, without impacting overall turnover.

Supporting different needs: a dual approach

While the case for a shorter, more concentrated core trading session is clear, James and Chris also acknowledge that Europe’s capital markets serve a wide spectrum of investors. This means flexibility still has a role to play, but it must reflect the varying needs of different investors.

Chris notes that institutional desks like Lazard’s focus on fundamental portfolio activity and client flows, not latency-driven strategies. “We’re not looking to trade at four in the morning,” he says. “That doesn’t help our clients. The vast majority of what we do is based on long-term portfolio decisions and client flows. Trading in a patchy market outside normal hours just isn’t useful to us.”

Still, he recognises that flexibility is important for some investor profiles. “There’s clearly a portion of the market that wants access beyond the core window,” he says. “But that doesn’t mean you extend the official session, it means creating mechanisms that serve retail in a structured way.”

This is where Europe’s infrastructure already offers a path forward. “We’ve seen flexible models in action,” says James. “In Germany, single-dealer platforms respond to overnight news and provide pre-market pricing across a wide range of names. We should build on that.”

Retail behaviour also differs by region. “Retail is probably around 5% of the market in Europe, compared to 20–25% in the US,” notes Chris. “There’s just not the same scale or structure of retail activity here. So building policy around the US model risks missing the mark.”

Both stress the importance of understanding who these participants are. A working parent with limited availability may benefit from extended access after hours. An institutional trader focused on liquidity alignment would not. Any structural change must reflect that diversity.

A European model, not an imported one

Neither James nor Chris is rejecting innovation. What they advocate is a purposeful evolution rooted in European market realities and investor needs.

They see this not just as a trading infrastructure question, but as of a broader effort to encourage engagement – especially among younger or newer investors. One of the French regulators recently highlighted how younger investors see crypto as less risky than equities,” James recalls. “That should be a wake-up call. It shows why education and perception matter just as much as access.”

For retail, that may include education, improved access to tools and greater flexibility during off-peak hours, without diluting core market integrity. For institutions, the priority remains execution quality. As Chris puts it: “Optimising the trading environment supports better outcomes for clients, and that should be the goal.”

A thoughtful way forward

Rather than framing the debate as a binary choice between longer or shorter hours, James and Chris point to a more nuanced, constructive path. Among the key takeaways:

- Align primary hours with natural liquidity formation to improve spreads and execution

- Provide optional mechanisms for retail participation outside core hours without diluting institutional focus

- Invest in education and tools to support long-term engagement from new and younger investors

- Base change on real data, test it, refine it and scale it only when it works.

This is not about resisting change, nor about copying global trends for their own sake. It is about shaping a market structure that reflects European realities and delivers better outcomes for all stakeholders.

As James and Chris make clear, progress does not lie in simply extending hours, but in understanding how Europe actually trades and building a framework that enhances liquidity, supports investor confidence and evolves with purpose.

“When 62% of volume trades in a two-hour window and overnight trading barely moves the needle,” says Chris, “you have to ask whether longer hours solve anything at all.”

James agrees. “This isn’t about being anti-change, it’s about being thoughtful,” he says. “It’s about understanding the dynamics in Europe and evolving in a way that protects both investors and market integrity. That’s what responsible leadership looks like.”

You may also like